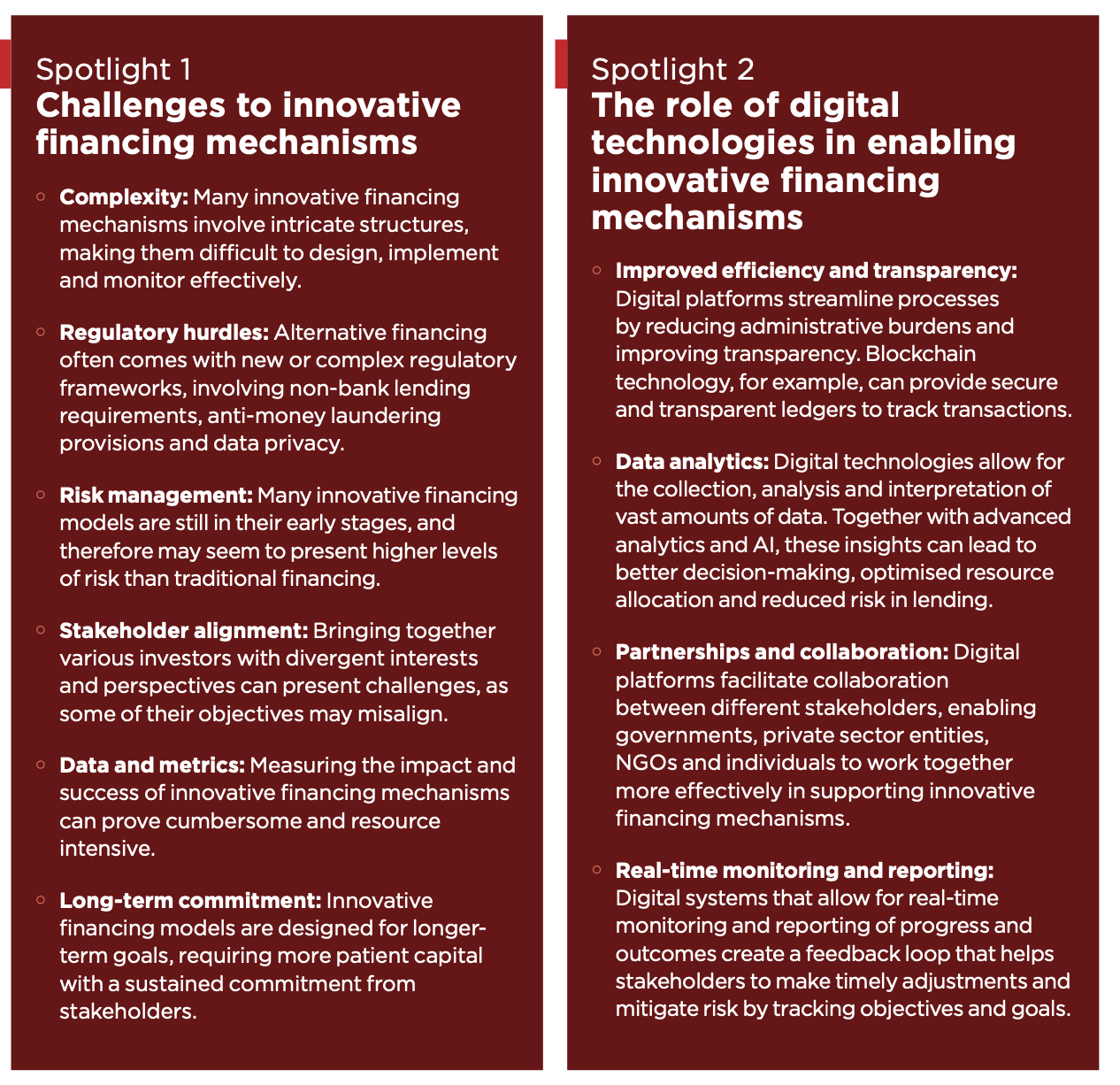

Digital technologies play a significant role in unlocking the potential of innovative financing mechanisms across the utilities sectors in Africa and Asia. Across these sectors, access to capital is a major challenge, particularly when enterprises have outgrown grant funding but do not have the scale to tap into traditional investment channels. Technologies like digital platforms, artificial intelligence (AI), blockchain and the Internet

of Things (IoT) can bring innovative financing instruments to the energy, water, waste, sanitation, recycling, mobility and asset-financing sectors. However, the scale of innovative finance has yet

to reach its potential, with only a small portion of available development assistance and sustainable private sector capital being mobilised through digitally enabled innovative financing.

There is little research that focuses specifically on the role of technology in unlocking innovative finance in the utilities service sector in low- and middle-income countries (LMICs). This research serves as a first attempt to categorise the complex value chain connecting upstream financiers exploring innovative financing instruments to

the midstream digital technology providers and solutions and on to the downstream implementers of utility service delivery and their beneficiaries.

The study uses novel conceptual and analytical frameworks designed to create a common language in identifying and analysing instances of digitally enabled innovative finance. The framework employs three distinct lenses that correspond to the principal stages within the value chain connecting financiers to implementers. This approach acknowledges that the frontier of innovation is continually expanding and context-dependent; what may be commonplace in one area can be considered innovative when applied elsewhere.

To operationalise this framework, each lens was defined through extensive desk-based research as well as consultation with key stakeholders.Limitations to this approach are principally around the interconnected nature of the different financial instruments and technologies which make categories less discrete in real-world applications than in theory. Nonetheless, the framework enables a complex landscape to be broken down into clear components.

Over 80 in-scope use cases were identified through this analytical framework. Use cases and their application of innovative finance instruments are segmented into mature, scaling and emerging categories based on the number of implementation examples documented in the literature, number of countries and sectors, and typical volumes associated with the instrument. These use cases serve to concretise the

universe of digitally enabled innovative finance instruments into a catalogue of examples where finance instruments, digital technologies and the transaction mechanisms underpinning them come to life in the real world. The study dives into five innovative finance instruments as case studies — receivables financing, alt-lending, climate, revenue- share models, and digitally-verified RBF – as a means to fully explore the relationship between digital innovation and these evolving models.

Key trends

Maturing use cases include social enterprises’

use of financial instruments such as alternative lending, receivables financing and crowdfunding. Digital technologies driving the growth of such

use cases principally include advances in satellite imagery and digital platforms that perform analytics on transaction and asset usage data enabled by IoT. Transaction mechanisms that foster the growth of these use cases include traditional mobile money and pay-as-you-go (PAYG) systems. The most mature use cases across the review were principally from the energy sector, with emerging innovation in the cooking space mirroring early successes of the PAYG solar lighting product and solar home systems (SHS) verticals.

Scaling use cases include those leveraging the growth of climate finance, revenue sharing models and digitally-verified results-based finance (RBF) mechanisms. The digital technologies principally driving these use cases are IoT systems paired with digital platforms capable of performing verification analytics, increasingly leveraging AI, and digital ledger technologies. Transaction mechanisms that foster these models include mass-payout electronic payment integrations into digital platforms, as

well as embedded finance mechanisms. Use cases exhibiting characteristics of scaling are largely focused on agritech and productive use asset- lending, particularly in the vehicle financing space.

Emerging use cases include social or environmental climate finance co-

benefits monetisation, impact bonds and

various applications of digital tokens and cryptocurrencies. These use cases increasingly leverage innovations in digital identity verification like biometrics and chatbots, as well as digital ledger technologies including smart contracts. Ledger technologies are particularly well represented in the transaction mechanisms underpinning emerging use cases. Emerging use cases were identified across sectors, with digital technologies surfacing as particularly prominent in use cases focused on the co-benefits of climate finance.

Accelerating adoption

Across the use cases considered, the most advanced and innovative organisations have pioneered a specific technology, instrument

or business model, layering on additional innovations with time. Enterprises or utility service providers aiming to leverage digital technologies to unlock innovative finance instruments

should master the technologies that produce tangible value in their sector, and consider what opportunities are offered by off-the-shelf solutions providers, particularly for IoT platforms, satellite imagery processing or blockchain solutions.

The intersection of climate and fintech finance

is an emerging macro trend that will likely

impact the landscape of utility service providers. Smartphone penetration and increasing maturity

in satellite imagery, IoT platforms, blockchain and AI are creating opportunities for utility service implementers to advance their digitisation journeys. Trends in mobile money interoperability and cross- border connectivity are also poised to unlock additional opportunities for building on PAYG models across Africa and Asia, particularly for receivables finance and climate finance.

Utility service enterprises need to recognise the value of digitisation in leveraging innovative finance. Digitisation processes typically begin with a desire to improve operations, with innovative finance opportunities often emerging as a byproduct. Developing a sector-specific understanding of which technologies are best suited to improving operations is often the first step towards tapping into the most appropriate innovative finance mechanisms.

Financiers across the impact-return spectrum need to leverage the data-sharing opportunities unlocked by digital technologies to generate sector standards. The use of innovative finance specific to the utilities sector is poorly characterised in the available literature. Grant, equity and debt financiers can leverage the exponential increase

in data generated by utility service providers to develop and share sector-specific benchmarks that can generate, benchmark and socialise both commercial and impact indicators.

Global corporations need to support transparent, and accessible financial intermediaries and instruments that can effectively allocate impact- oriented capital flows. Increased attention on corporate climate and ESG impact metrics means that corporations need to drive digitally enabled mechanisms that can enable standardised, timely, and reliable impact data.

Mobile network operators (MNOs) have a key

role to play across the landscape of use cases. Increased attention to utility verticals represents

a significant opportunity for operators to

develop additional revenue streams and move towards a positioning as a technology partner for organisations in the ecosystem. Laser-focused attention on facilitating third-party access to mobile money integrations across markets can additionally support utility service providers’ ability to digitise operations in their financing journeys.

Partnership opportunities highlighted through the landscape emphasise the need for blended finance. Development financiers and impact- oriented investors can unlock new private capital by de-risking investments into technology- enabled sectors through guarantee mechanisms and concessional forms of investment. Such partnerships represent the opportunity to include novel players like local banks and public agencies in pioneering otherwise poorly understood financial instruments across new geographies.

Achieving an inflection point in innovative finance using technology will require dedicated efforts in breaking down silos across the investment landscape. The returns on investing in digital innovation can take years to be realised, and typically require time and effort to understand for those not already immersed. This report serves to capture some of the most significant intersections of technology and finance trends that will guide the needed deployment of climate-resilient, pro- poor capital in the utility service sectors in the coming decade.

You must be logged in to post a comment.